Fun fact: I took this picture at the top of Sulphur Mountain in Banff the day I proposed to my wife. She passed the challenge of climbing to the top (no gondola allowed), so she was rewarded with a ring. Now she has to put up with me for the rest of her life!

Fun fact: I took this picture at the top of Sulphur Mountain in Banff the day I proposed to my wife. She passed the challenge of climbing to the top (no gondola allowed), so she was rewarded with a ring. Now she has to put up with me for the rest of her life!

I thought I would take the chance to run through what coaching the average Canadian Household would look like. Through this process, I hope to give my audience a preview of what part of my financial coaching program looks like and some ideas of how they can make positive changes to their own personal finances.

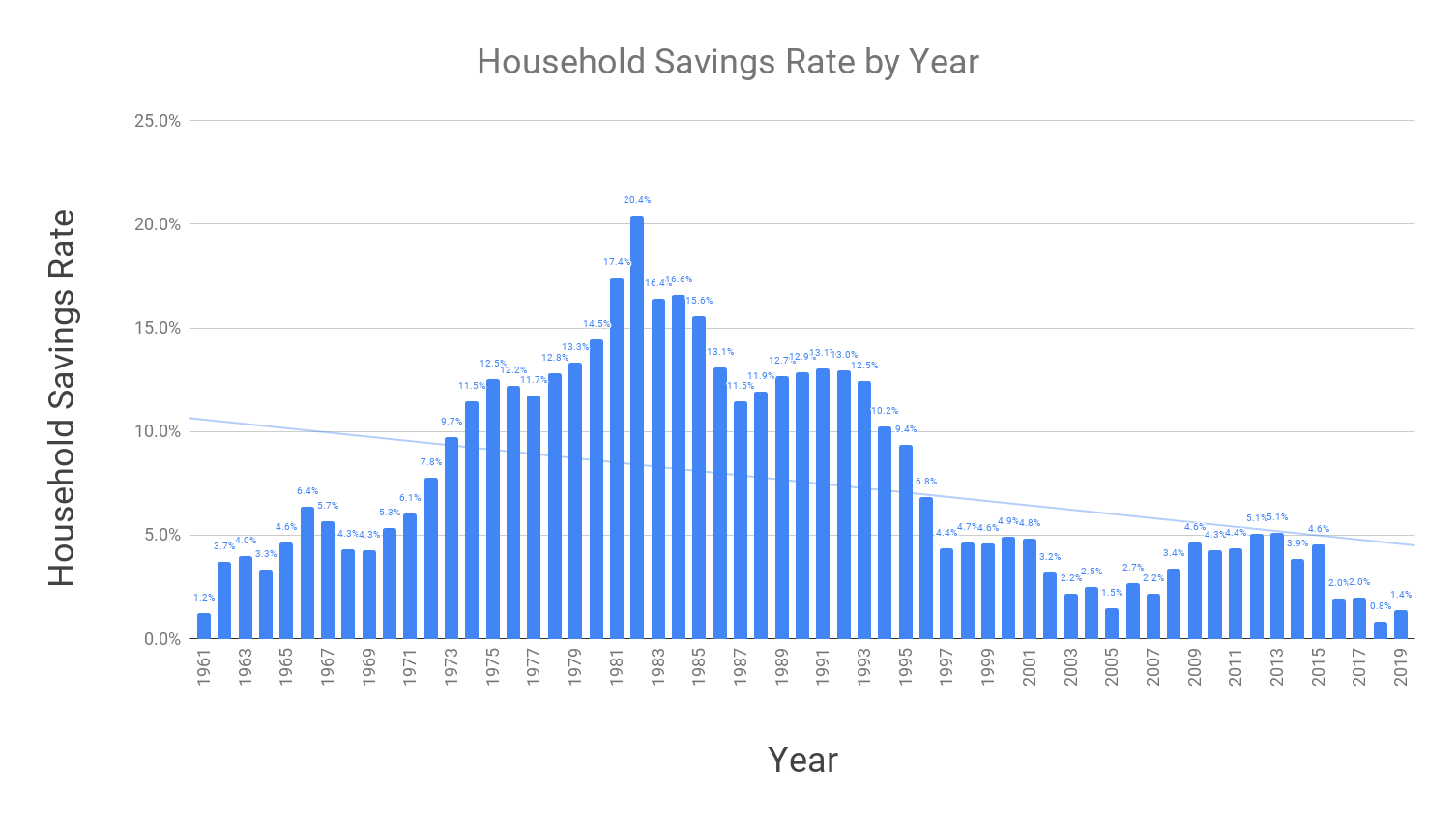

As discussed on my homepage, Canadian’s aren’t saving enough! Here is the proof:

I know, the chart is small and hard to read. Let me give you a few highlights:

- The average savings rate has been trending down for decades (see blue trend line)

- The 2018 savings rate was the lowest on record since 1961

For a chart you can actually read, let’s just look at the last 10 years.

Key observations:

- Savings has dropped substantially in the last 10 years

- Savings rates recently are nowhere near where they need to be for Canadians to reach financial independence! This means that the average Canadian will likely have to work longer and rely on Canada Pension and Old Age Security in their older years to get by.

It is my sincere hope for the average Canadian Household to increase their savings rate since you know from a previous post that savings rate is the most important financial metric that will determine if and when you reach financial independence.

Please note that this analysis is based on data from Statistics Canada. This analysis is not perfect because there are certain limitations to using average data. For example, it assumes the average household has 1.23 kids, rents 44% of their home and owns the other 56%, drives 1.5 cars, etc. Obviously this doesn’t make sense, however, let’s look past these limitations for now and just focus on the big picture – the fact that Canadians aren’t saving enough.

Part 1: Tracking the Average Canadian Household Finances like a Business

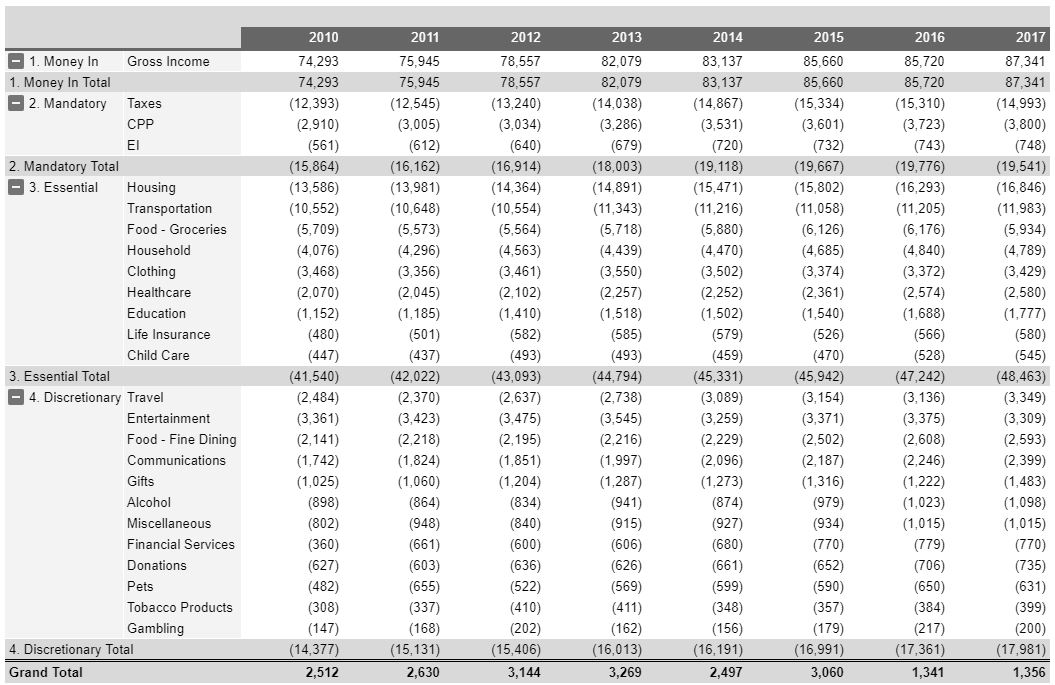

Generally after the free consultation / meet and greet session, the first thing I like to do with my coaching clients is to start tracking their finances like a business. I’ve detailed some of what I like track in this post. For most people, it takes a couple months to get used to tracking expenses and start to get some meaningful data. In this case, for the average Canadian Household, data is plentiful so I was able to get 8 years of data. Here is what I came up with:

Income & Expenses Table

I was able to leverage my personal finance geek / spreadsheet skillset to come up with the table below that succinctly details the average Canadian Household’s income and expenses. As you can see, income is positive, expenses are (negative) and the “grand total” at the bottom represents savings -unfortunately not so “grand” in the case of the average Canadian Household.

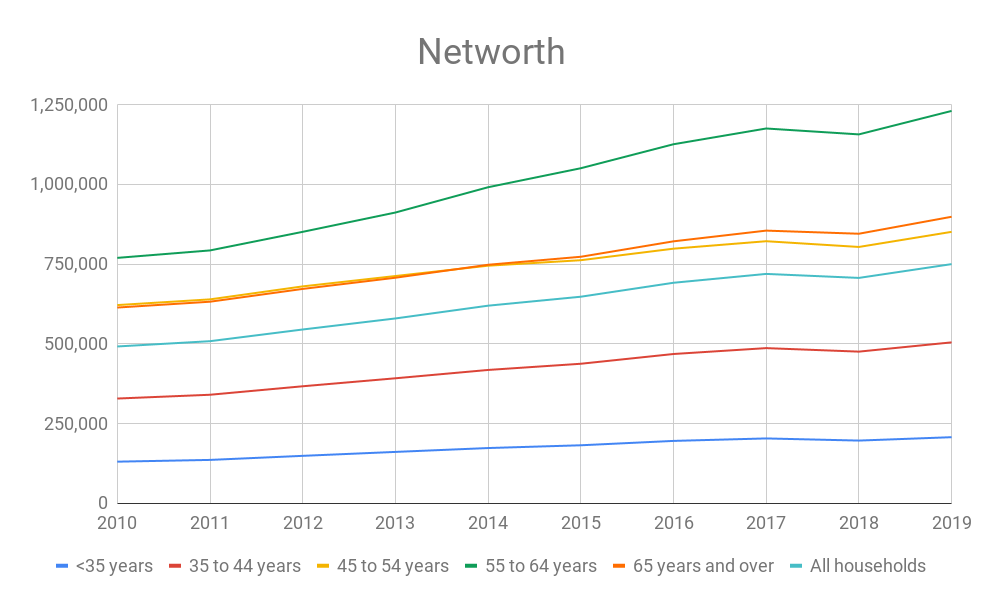

Networth Chart

Another important metric I encourage my clients to track is networth (that is, total assets minus total liabilities). This is a good measure of total wealth that can be very motivating to track over time. Here is where the average Canadian Household came up on networth (grouping in to different age groups and the overall average):

Financial Independence Chart

The following is what I like to call the “Financial Independence Chart”. It visualizes the subtotals from the four categories in the Income & Expenses Table above and overlays a green line that shows how much of the client’s expenses would be covered if their networth was invested at a 4% annual rate of return. As you can see, if the average Canadian’s networth was invested at 4% return, the investment income wouldn’t even cover their essential expenses, let alone their total expenses (what is required to reach financial independence).

Summarizing the data table and charts above – the average Canadian Household, in 2017 had:

- Gross income of $87,341

- Paid $19,541 in taxes, CPP, and EI (22.4% of gross income)

- Spent $48,463 on essential expenses (55.5% of gross income, or 71.5% of net income)

- Spent $17,981 on discretionary expenses (20.6% of gross income, or 26.5% of net income), and

- Saved a measly $1,356 (1.6% of gross income, or 2.0% of net income )

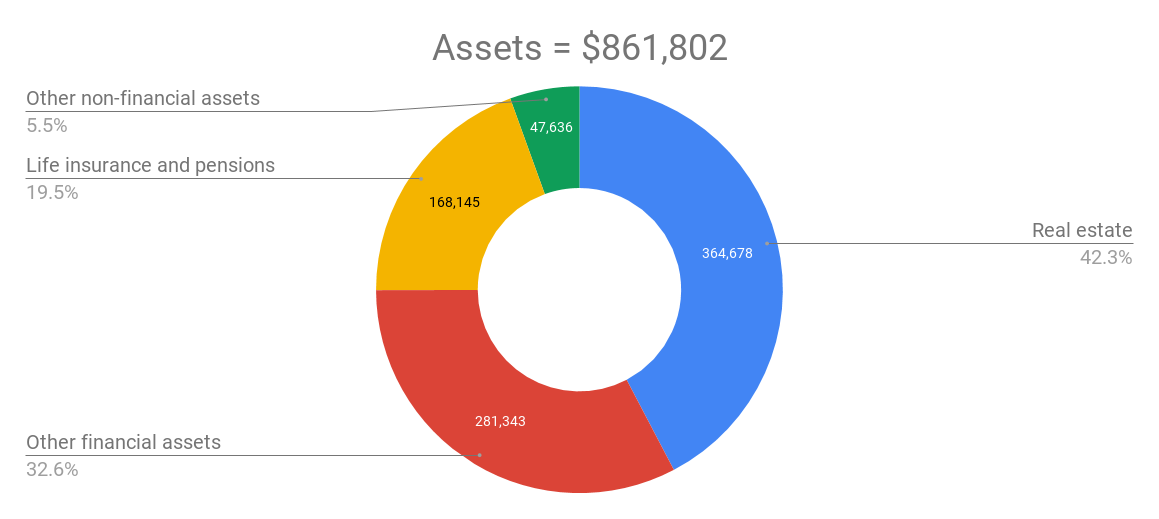

- Networth breakdown:

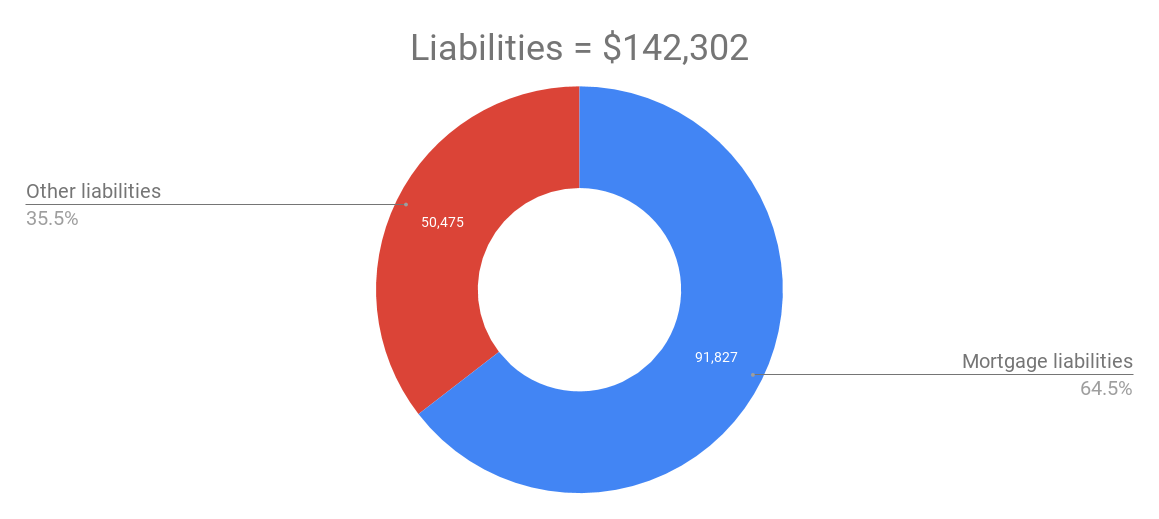

Networth = Assets $861,802 – Liabilities $142,302 = $719,500

After reviewing the data and charts above, I come to a few preliminary conclusions:

- Based on the average net savings rate of 2%, ignoring CPP and OAS, the average Canadian household would have to work 77 years to reach financial independence

- Real estate represented 42.3% of total assets and 50.7% of networth

- It’s important to note that from a portfolio perspective, you should think about your real estate exposure as the total value of the real estate assets (not just the equity amount after deducting your mortgage) divided by your total networth (not total assets). In my opinion, having 50%+ of your networth in a single, illiquid real estate asset in a single market is risky and limits your ability to invest in other investments that are likely to outpace real estate. This is part of why I decided to rent vs. buy in my early 20’s and held off on buying a house until my early 30’s

- Most of the data used above is based on the “Average Canadian Household”, however, I also have the ability to cut the data by age group and income quintile. I couldn’t resist looking at the break down by age group here:

- What I found was that households in the “less than 35 years” age bracket on average had real estate assets that exceeded their networth! 104% to be exact (using 2017 numbers)

- This means that the average young household in Canada is extremely exposed to real estate. That’s all fine and dandy when real estate is booming, however, a retraction in real estate could really deal a blow to these young households (don’t forget if real estate depreciates, the “asset” on your personal balance sheet goes down, but your mortgage doesn’t!). Not to mention that these young households are probably pouring most of their capital into servicing mortgage debt and other expenses that come along with home ownership. In some cases, this forces young households to take on additional consumer debt to cover other expenses (higher interest credit card debt, etc.)

- I am a bit concerned about the $50,000+ of “other liabilities” as this is likely high interest consumer debt (student loans, credit cards, unsecured lines of credit, payday loans, etc.)

- Digging further into the data here, and not surprising, younger households and lower income households have a higher percentage of “other liabilities” relative to their overall networth

- Based on the amount of tax the average Canadian pays (combined with the low savings rate), it is likely that they aren’t taking advantage of various tax-advantaged accounts that could save them a significant amount of tax expense (specifically, Registered Retirement Savings Plans and Tax-Free Savings Accounts)

- Both the fixed and discretionary expense categories seem high relative to total income – this suggests the need to earn more and/or spend less.

There is a lot of room for improvement in the average Canadian Household’s finances. In my next post, I’ll go through some action steps that could be taken to reduce essential expenses.

Here’s what I have planned for the 6-part series:

Part 1: Tracking the Average Canadian Household Finances like a Business (what you just read)

Part 2: Aligning Essential Expenses with Values

Part 3: Aligning Discretionary Expenses with Values

Part 4: Aligning Earning with Values

Part 5: Constructing a Savings and/or Debt Paydown Strategy

Part 6: The After Picture – How the Average Canadian Household’s Finances Might Look like After JBFI Financial Coaching

If you are interested in my Financial Coaching Program, get more information on the program here and sign up for your free consultation.

Sources:

- Income and Savings: Distributions of household economic accounts, income, consumption and saving, Canada, provinces and territories

- Spending: Household spending, Canada, regions and provinces https://www150.statcan.gc.ca/t1/tbl1/en/cv.action?pid=1110022201

- Networth: Distributions of household economic accounts, wealth, Canada, regions and provinces, annual

- https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610058601&pickMembers%5B0%5D=1.1&pickMembers%5B1%5D=2.3&cubeTimeFrame.startYear=2015&cubeTimeFrame.endYear=2019&referencePeriods=20150101%2C20190101

Pingback: Financial Coaching the Average Canadian Household (Part 2 of 6) | JBFI Inc.

Pingback: Financial Coaching the Average Canadian Household (Part 3 of 6) | JBFI Inc.

Pingback: Financial Coaching the Average Canadian Household (Part 4 of 6) | JBFI Inc.