Part 3: Aligning Discretionary Expenses with Values

This is the third post in a series of six that walks through a theoretical exercise of me financially coaching the Average Canadian Household (as defined by Statistics Canada data) to see how we could improve their financial situation.

In the first post, we did a deep dive into the Average Canadian Household’s finances, looking at their income, expenses, and net worth.

In the second post, we did a deep dive into the Average Canadian Household’s essential expenses. Now on to discretionary expenses.

What do I mean by discretionary expenses? If essential expenses are the “needs” (recognizing that our essential expenses often go way beyond our basic needs), discretionary expenses are the “wants”. These are things that (hopefully) add value to our lives beyond the basic needs. Everyone has very different views on where they should spend their money in discretionary categories and everyone is different. I’m not here to judge anyone, more just to make sure that their spending is aligned with their values. People need to understand that they are ultimately trading their time to buy stuff or experiences, so the stuff or experience better be worth it!.

It’s not about deprivation! But being in debt can be a unique circumstance

I’m not the kind of financial coach that is going to tell you to stop buying your $5 coffee every day. I’m all for it it as long as you get value from it. That said, I believe that if you have outstanding high interest consumer debt (e.g. credit cards, payday loans, etc.), it may warrant cutting back on discretionary expenses temporarily in order to disentangle yourself from that vicious web as soon as possible. Every extra dollar that you can put towards your debt load counts and small amounts add up over time. The financial independence blogger, Mr. Money Moustache wrote a great post about referring to debt as an “emergency”. Here it is: https://www.mrmoneymustache.com/2012/04/18/news-flash-your-debt-is-an-emergency/.

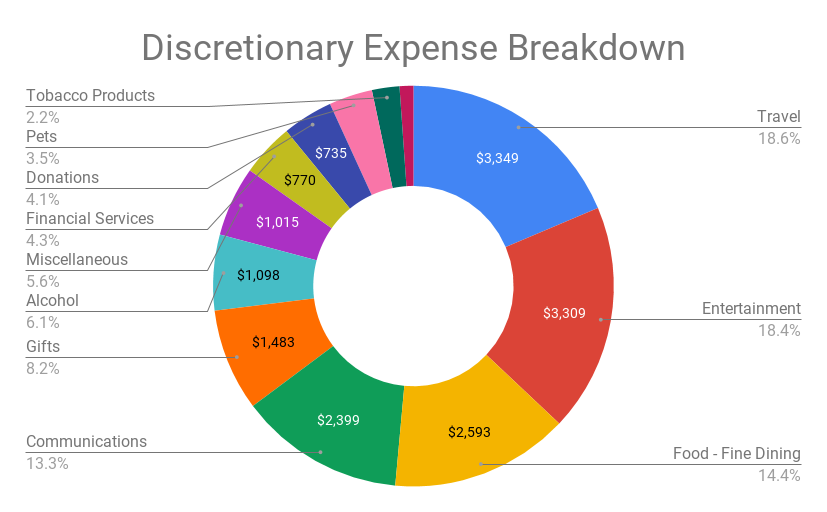

Here’s the breakdown of discretionary expenses for the Average Canadian Household (based on Statistics Canada data):

Travel

- I am actually happy to see that travel is the #1 discretionary expense category for the Average Canadian Household. I love to travel and think that travel expense is closely aligned with the values of many Canadians.

- General savings tips on travel:

- For flights, I use google flights

- This allows you to find the lowest prices across various airlines

- Generally, I find you can save a lot of money if you can be flexible with your dates (e.g. for a vacation, sometimes you can save significantly on flights if you depart and arrive mid-week rather than on a Saturday or Sunday when everyone else is travelling)

- Accommodation

- I look for the best hotel deals on an aggregator site like Expedia or Booking.com

- I have had great success staying in Airbnb places as well. It is often similar or cheaper than staying in a hotel. In my experience, you get a lot more space (relative to a hotel room) plus the added benefit of meeting other people. Every host that I have stayed with using Airbnb was fantastic and really gave me a sense of how it is like to live in different areas throughout the world

- These aren’t for everyone but can be very budget-friendly alternatives:

- Hostels – I love staying at hostels because I find I meet so many new people. This isn’t for everyone, but that’s okay. There are hostels everywhere, particularly in expensive cities

- Camping – I’m a big fan of the outdoors and will often choose sleeping outdoors over inside

- Package trips

- Sometimes you can save a bundle buying a package trip that includes flights and accommodation. I did a few of these during university and my early working years for a quick and easy getaway to a sun destination. It’s sometimes nice to book everything as a package to avoid the analysis paralysis associated with booking flights and accommodations separately

- Travel rewards

- I’m a big fan of using credit cards that give me reward points or cash back for travel purchases. This isn’t for everyone and I would only recommend doing this if you can pay your credit card off in full every month. If you can’t pay off your credit card in full every month, I don’t recommend using it as the interest charges will likely outweigh any benefit that you will get from points. My travel expenses have been significantly reduced from using travel reward dollars

- Loyalty programs

- Most airlines and hotel chains have loyalty programs. If you travel a lot, it really makes sense to sign up for the loyalty programs as the benefits can accrue quite quickly. Sometimes loyalty points and travel rewards from credit cards are also interchangeable / exchangeable

- For flights, I use google flights

Entertainment

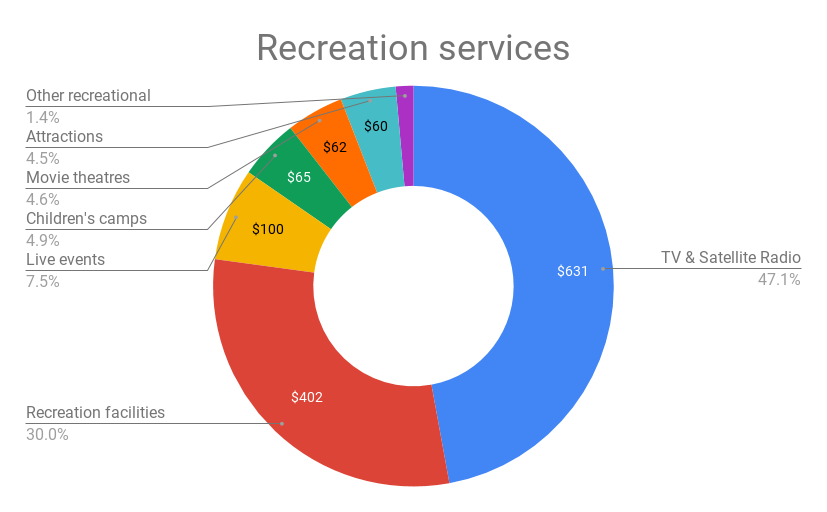

- Recreation services

TV & satellite radio

TV & satellite radio

- Consider switching from more expensive cable TV package to less expensive streaming services like Netflix / Prime Video / Disney Plus

- I don’t watch a huge amount of TV but a good show or movie can be a great way to unwind!

- Recreational facilities

- I know a lot of people love going to the gym and other recreational facilities (for the exercise benefit and social interaction with others). I prefer to do most of my workouts outdoors (hiking, walking, cycling), but occasionally enjoy the gym, especially in the middle of winter! Some people are guilty of signing up for gym memberships and hardly using them – if you are one of them, use it or cancel it!

- Live events

- Concerts and sporting events can be a great way to spend money and something that can provide lasting memories

- Electronics

- With most electronics, rather than buy the latest and greatest, I usually consistently stay a couple years behind the newest technology. This can save you big bucks. For example, the newest cellphones right now are around $1,500, however you can get a brand new older model for less than half of that price. Same goes for TV’s, computers, etc. I absolutely don’t feel deprived or like I’m missing out by using an older model

- Recreational vehicles

- I’m not a huge fan of RV’s (more of a tent guy myself) and various toys (e.g. boats, ATV’s) but I know many Canadians get tremendous value from these purchases. The only thing that I would say here is to make sure that you consider rent vs. buy (whether you will get enough use out of these items every year to justify the capital required and additional work associated with owning these items – e.g. maintenance, storage, etc.)

- I would love to get a motorbike but unfortunately both my mom and my wife are against it. I know better to mess with these two women!

- Reading materials

- I’m personally a big fan of the library – a good way to save money on reading material and avoid cluttering your home with hundreds of books

Food – Fine Dining

- The average Canadian Household spends just over $200 a month eating out at restaurants. I don’t think that average sounds bad at all. I quite like eating out occasionally. My general principles are:

- If I can do it better at home for less – do it! For me, this applies to most things barbecued. It pains me to pay $40 for steak at a restaurant if it isn’t cooked to my liking. For other things that I don’t know how to make, or would take too much time to prepare, or would have to spend a lot to buy the ingredients (e.g. sushi), I am always happy to go out and pay for these meals

- Don’t eat out alone (unless you enjoy it) – part of eating out for me is the company / social aspect, so I generally don’t eat out alone

- Only eat out occasionally – I find that I enjoy eating out more if I only do it once or twice a month. That’s just me since I find that if I eat out too regularly, it just becomes the new normal

Communications

- Canadian’s pay WAY to much for communication (cell phones, home phones, internet) due to the oligopoly that exists with the big players (sometimes I really think they collude and raise their rates in tandem), the geographic sprawl of the country, and the low population density relative to other countries. There have been studies done that show that Canada has one of the most expensive rates for wireless voice and data rates

- The Average Canadian Household pay over $100 per month for cell phone alone

- I have heard of many people that pay over $200 per month for a single cell phone plan! I definitely recommend looking at cheaper alternatives. There are certain companies (e.g. Public Mobile, Fido, Koodo) that offer much cheaper plans than the big players (Telus, Rogers, Bell). These alternatives often provide the exact same service as the big players for a lower cost (mostly because they are owned by the big players)

- Same goes for internet – there are cheaper plans available from smaller companies that use the same networks that the big players use. I recently switched my internet service to Lightspeed from Telus. Doing this, I was able to save more than 40% and get a faster service compared to what I had with Telus.

Gifts

- I personally get a lot of value in gift-giving. This is probably one of those categories where you can spend relatively guilt-free. That said, you have to make sure you are keeping within your means – for example, maybe don’t buy your kid a car if you have significant consumer debt that is dragging on your own financial situation. If your strapped for cash, less-expensive sentimental gifts can go a long way and can sometimes mean more to the recipient than something material or expensive.

Alcohol

- In my younger years, I spent a significant amount of money on drinking especially at bars and restaurants. In hindsight, I wish I had poured that cash into index funds instead! That said, live and learn – was fun while it lasted. The mark up on alcohol at restaurants is among the most ridiculous (e.g. paying $10 for a beer, or $13 for a glass of wine when you know you can buy the bottle for less than $10 at a retail store). When you do drink out with your buddies, watch out for deals, e.g. 1/2 price wine Wednesdays, happy hour, etc.

Financial Services

- There is no need to pay for financial services. I’ve never paid a bank fee or interest charge in my life. There are a couple options here for low-cost / free banking:

- Go with a no-fee chequing / savings account like Tangerine or Simplii

- Go with a full service bank that will waive the monthly fee for a chequing account if you maintain a certain minimum balance. This is what I chose to do – I have TD’s best chequing account and don’t pay the ~$30 monthly fee since I maintain a minimum balance of $5,000 at all times. I realize that there is an opportunity cost to having that $5,000 tied up, however, I do feel that the other benefits that I get outweigh the costs (e.g. annual fee waived on my TD First Class Travel Visa card, free safety deposit box, free bank draft and cheques whenever I need them, unlimited transactions, etc.)

Donations

- I think donation is a very important discretionary expense that most people should try to increase over time as their wealth accumulates. Don’t forget to keep the receipt if the donation is tax deductible since it can save you some money during tax season

Pets

- This is expense category that I’m not going to mess with. I know of many people who love their pets like children. I think pets can be a very worthwhile discretionary expense as far as bringing happiness to lives

Gambling

- I would advise that you only gamble occasionally for entertainment and only in small amounts that you are 100% okay with losing if things don’t go your way. I personally enjoy playing a little bit of Blackjack when I’m in Vegas (at least there you get the benefit of free drinks!)

Tobacco

- I don’t smoke, so don’t have too much to say here. I do have family members and friends who quit smoking and noticed significant financial and health benefits by doing so. That said, some people truly get enjoyment from smoking and choose to do so regardless of health and financial implications. To each their own

At this point, we have analyzed the Average Canadian Household’s financial situation and talked about potential ways to decrease essential and discretionary expenses. I view decreasing expenses as playing defense. There is only so much you can cut without depriving yourself. To have a happy life, you need to figure out what level of expenses are right for you (not so high that they will impair your ability to save for financial independence, but not so low that you feel deprived and not enjoy the journey). Next post, we will talk about playing offence by earning more money. Whereas the amount of expenses you can save is limited, there is no cap on the amount of money you can make!

If you are interested in my Financial Coaching Program, get more information on the program here and sign up for your free consultation.