As I wrote my last post on My take on rental properties, it got me thinking about another related topic – the question of whether to rent or buy a house.

For the average household, housing is the second largest expense (after tax of course). That said, it is important that we all spend some time thinking about our decision to buy a house or rent.

Most people assume that it is always better to buy if they have the means since they’ve probably been told one of the following:

- If you rent, you are just throwing money away / paying your landlord’s mortgage

- You better buy, so you can build equity!

- Home prices only go in one direction – that is UP! So don’t miss the boat

There is a great book I read a few years ago that goes through this decision in quite a bit of detail – it is called “The Wealthy Renter”. It goes through the decision in a lot more detail than I plan to go through here.

The common “myths” above imply that owning is always the optimal decision, however, it is important that we run the numbers to ensure this is true. Home selection (especially when deciding on a primary residence) also goes beyond the financials – there are other emotionally driven factors that we should consider.

First, let’s weigh some of the pros and cons of owning and renting:

- Pros of owning:

- You have a home that is truly yours that you can do whatever you want with it

- You can’t get evicted from your own home (as long as you can make the mortgage payments!)

- Forced savings – for those who are not disciplined in saving money, owning a home and making mortgage payments “forces” you to save and build equity (through the initial down payment and the ongoing principal portion of the monthly payments)

- Potential for appreciation of home value

- Cons of owning:

- Significant upfront and ongoing financial commitment

- Significant real estate market exposure (often people, especially young people, will buy a house that has a value that is greater than their total net worth). This seems okay because everyone is doing it, however it is pretty risky from a portfolio diversification perspective

- Significant transaction costs – you have to pay a lawyer every time you buy or sell a property, and potentially a realtor when you sell a property

- Ongoing maintenance costs – roof, windows, plumbing, furnace, etc.

- Annual property tax – for example, 0.9% of the property value every year in Edmonton

- Illiquid asset – can sometimes take a while to sell a property

- Potential for depreciation of home value

- Renting pros:

- Lower financial commitment

- Can invest the money that would otherwise be tied up in home equity

- Flexibility to move/ travel for an extended period of time without having to worry about selling a house

- Option to try out different neighborhoods

- Switch from place to place without incurring significant transaction costs

- Renting cons:

- Don’t get that warm / fuzzy feeling from owning your home on your own land

- You can be forced to move at a time that’s suboptimal for you if your landlord chooses to vacate you

- Less flexibility to “make it your own” – your landlord might not be as excited about orange walls as you are

Now on to the financial analysis:

As I stated in my previous post on “My take on rental properties“, my wife and I are currently renting a 2 bedroom, 2 bathroom apartment. Since we recently had our first child, we too have been talking a lot about moving into a house, and whether we want to rent or buy. As part of this analysis, I built a comparison tool using Google Sheets.

- To do this analysis, I picked a house for rent in Edmonton and compared the “renting” scenario to the “buying” scenario

- Renting assumptions

- Cost to rent (per month) = $2,100

- Tenant insurance (per month) = $50 (tenant insurance is generally less than homeowner insurance since you are only insuring the contents rather than “contents + structure”)

- Buying assumptions

- Property value: $643,000

- To find the value of a house, I checked the City of Edmonton’s property tax appraisal website (https://maps.edmonton.ca/map.aspx?lookingFor=Assessments\By%20Address). The property tax appraisal value is not always equal to the market value of the property, but is generally a good proxy

- Annual property tax: $5,996 (0.9% of the property value per year, $500 / month)

- Also available online for Edmonton: http://taxestimator.edmonton.ca/

- Time horizon: Let’s assume we plan to hold this property for the long term (say 20 years). Generally a longer time horizon makes the economics of owning more favourable since one-time costs will be amortized over a greater number of years

- Mortgage: for now let’s assume that we use leverage since this is the norm for most people buying a home. Assumptions:

- Down payment: 10%

- Mortgage term: 20 years (let’s assume the mortgage is completely paid off by the end of the time horizon to make the math easier)

- Mortgage rate: 3.50%

- I know interest rates are low right now, however, we need to consider what our borrowing costs may be over a longer term. As far as I know, unlike the US, it is quite rare to get a 25-year fixed rate mortgage in Canada

- Appreciation: per my last post on rental properties, the appreciation over and above inflation over a 40 year time horizon in Edmonton was 0.5%

- I would be careful about including significant inflation over and above the rate of inflation. The price of housing in real terms (adjusted for inflation over time) will fluctuate based on the supply and demand for housing in each region / community. Let’s also not forget that past performance is not indicative of future performance. Just because one neighborhood or city may have had significant appreciation over and above inflation historically, it doesn’t mean that this will continue forever

- Maintenance costs: $4,500 / year (works out to ~0.7% of the purchase price per year)

- Per the following article from Money Sense Magazine, “The total amount you should budget for home maintenance: $4,500 – $10,000 per year”. The lower end of this range seems suitable for the example I’ve chosen

- https://www.moneysense.ca/spend/real-estate/the-ultimate-home-maintenance-guide/

- Taxes: Given there is a principal residence capital gain tax exemption in Canada, there is no tax payable on capital gains on your principal residence. Unlike the US, mortgage interest is not tax deductible in Canada

- Realtor cost to sell: 3.0%

- I’ve read that the typical range is 3-7% in Canada

- Legal costs to buy and sell: $1,000

- Homeowners insurance: $150 / month

- Property value: $643,000

- Common assumptions (applicable to both the buy and rent scenarios)

- Utilities: $350 / month (for power, water, gas, and garbage pickup)

- Inflation: I have excluded inflation in this example so everything is based on real terms

- Renting assumptions

Results of the analysis:

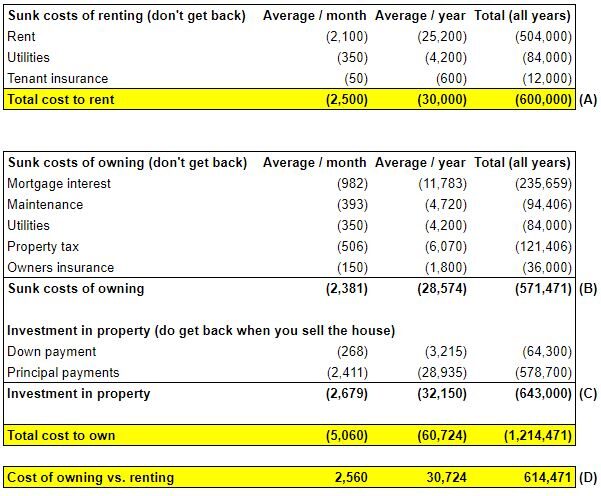

When comparing the cost of renting to the cost of owning, it is clear that renting is significantly cheaper in this example:

- Total cost to rent over the 20 year time horizon = $600,000

- Total cost to own over the 20 year time horizon = $1,214,471

- At first glance it appears that renting is cheaper than owning by $614,471 over a 20 year period

Now this isn’t exactly fair, why? Because there is a big difference between what the renter has at the end of the 20 years and what the owner has:

- The renter has $0 (when he moves out, he gets his security deposit back from the landlord and moves on)

- The owner has a house at the end of the investment period!

- Recall that the owner paid $643,000 for the house

- At the end of the 20 years, the house is worth $710,448 (recall that we said the house appreciates at a rate of 0.5% over and above the rate of inflation)

- We said that the owner would pay 3% to a realtor to sell (3% x $710,448 = $21,313)

- We said that the owner would pay $1,000 in legal costs when selling the property

- The net proceeds from a sale would be $710,448 (-) 21,313 (-) = $688,134

Recall we initially said that renting was cheaper than owning by $614,471. Now if the owner were to sell the house at the end of the 20-year period, he would receive $688,134 based on the assumptions above – effectively making them better off owning (see calculations below).

- Adjusted cost of ownership =

- Total cost to own from table above = ($1,214,471)

- (+) sale proceeds of house = $688,134

- Total net cost to own the house = ($526,337)

- Comparing to the total cost to rent over the 20 year period ($600,000), it now looks like owning is ahead by $73,663

Now this is more in line with traditional beliefs that owning is less expensive than renting in the long term. That said, we are still ignoring one very significant consideration – the fact that when you own a house, a significant amount of capital is tied up in the equity of your home. If you are a renter, rather than this equity being tied up in your home, you can invest the excess cash.

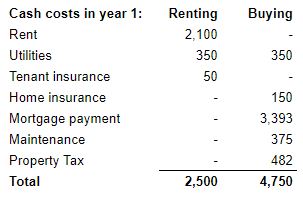

The cash required to own a home is significantly higher than renting:

- Initially – when you first buy a home, you are required to fund a down payment (generally 5-20% of the market value of the home). This amount is significantly more than the up front cash required to rent, generally just a one-month security deposit.

- Ongoing – Your monthly cash requirements are also much greater when you own a home. This is due to the fact that there are significant sunk costs (that you will not get back) when you own a home (e.g. mortgage interest, property tax, maintenance, insurance).

- As you can see, the monthly cash cost of buying a home ($4,750) is almost double what it costs to rent ($2,500)

For a true apples-to-apples comparison, let’s say that the renter invests the excess cash. Assume that the renter can invest the excess cash at an after-tax return of 3% over and above the rate of inflation (a conservative assumption given that it is below historical returns for a balanced portfolio).

- Initially, the renter invests the same amount as the buyer’s down payment

- On a monthly basis, the renter invests an incremental ~$2,250 (the amount of cash it costs to own over and above what it costs to rent)

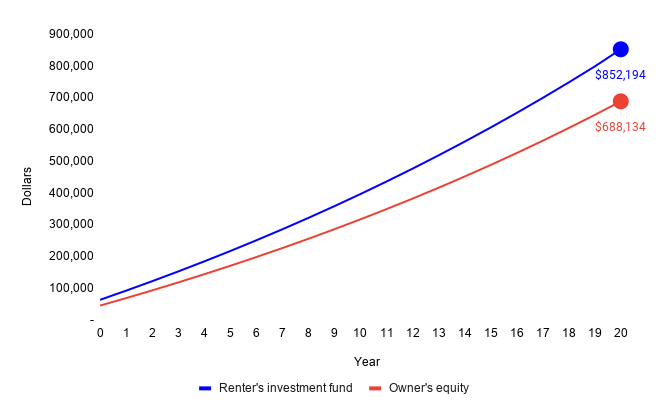

Now let’s look at the numbers again at the end of the 20 year time horizon:

- Red line: Recall the owner had net proceeds of $688,134 from selling the house

- Blue line: The renter, given that he invests the excess cash in other investment instruments yielding a 3% return, would have $852,194 in his investment account

Now let’s look at the total net cost of renting vs. owning:

This implies that renting is $164,060 cheaper over the 20-year time horizon ($684 / month).

Going back to the reason for writing this post, ultimately what we want to find out is whether it is financially more sensible to rent or to buy. When you buy a house, in addition to the sunk cost of home ownership, you also invest equity in the house (initial down payment and principal payments on the mortgage). It is important to consider that if you chose to rent instead of buy and you invested the cash differential, you could be significantly better off (assuming a 3% return on your investment portfolio vs. 0.5% home value appreciation – disregarding inflation). These assumptions reflect the fact that a balanced portfolio of stocks and bonds has generally outperformed average residential real estate appreciation historically.

Quickly, a comment on each of the myths stated at the beginning of the post:

- If you rent, you are just throwing money away / paying your landlord’s mortgage

- Not necessarily true – as you can see now, the sunk costs of home ownership can be close (or higher in some cases) than renting

- In this example, the sunk costs of owning the home (which are not recoverable) average $2,381 / month (close to the $2,500 all-in cost to rent)

- You better buy, so you can build equity!

- You can build significant equity by renting – IF you are disciplined in saving to invest the excess cash that you would have otherwise paid to own. Furthermore, you can choose to invest in a more diversified portfolio (e.g. stocks / bonds / ETFs) that potentially has less risk than a single real estate investment in a single market. A portfolio of public investment securities would also have superior liquidity, given the lower transaction costs and higher ease of converting the portfolio into cash when needed

- Home prices only go in one direction – that is UP! So don’t miss the boat

- We all know this was disproven during the 2008 global financial crisis where homes in certain locations decreased in value by 50%+

I’m not saying that renting is always better than buying. The single biggest takeaway from this post is that when you are comparing renting vs. buying, you need to compare apples-to-apples and take in to account ALL factors, including investment income that a renter could earn by investing the cash that he doesn’t have to fork out for a down payment and more expensive monthly expenses along the way.

Like everything else in personal finance, the decision to rent or buy is very personal and there is no right answer. A financial optimizer may look to do whatever the numbers say, however, somebody who prioritizes other qualitative factors in their decision may have another view.

My wife and I chose to rent an apartment for now (mainly because we valued the close proximity to work and didn’t value a yard or a bigger living space before having kids). We will look to purchase a house eventually, not only because the numbers are likely to look favourable with a longer time horizon, but emotionally, we do want to own a house – a place where our family can truly make our own.

Either way, I think you should at least look at how the numbers stack up before making your decision between buying and renting. For many of us, this is usually the largest financial decision of our lives. As usual, if you would like help running the numbers, or just to chat/debate on this topic, feel free to reach out to me at jonathan@jbfi.ca.

Pingback: Ideas to Reduce Transportation Expenses – JBFI Inc.

Pingback: We bought a house! | JBFI Inc.

Pingback: Financial Coaching the Average Canadian Household (Part 2 of 6) | JBFI Inc.

Pingback: Financial Coaching the Average Canadian Household (Part 1 of 6) | JBFI Inc.