This is one of those posts that might stir the pot in the financial independence community. I want to be clear that I am certainly not opposed to real estate investing, I just think that people need to be careful and fully aware of the various risks associated with real estate investing before they dive in head first and buy six properties. I personally have not made any real estate investments (other than Real Estate Investment Trusts and the purchase of my principal residence) to date, however, I may look to do so in the future if I find a rental property that has a risk adjusted return that I think is high enough to justify the market exposure and illiquidity. I’ve seen a lot of people in the personal finance community succeed with real estate investing, in addition to those who invest in traditional asset classes and run their own businesses.

I’ve spent most of my career working in institutional private investments where a large portion of my time is spent performing due diligence on potential investment opportunities. Applying my institutional investment knowledge to smaller retail investments (such as rental properties) gives me an interesting perspective.

Why does everybody think real estate is such a good investment?

- Short answer – real estate always goes up (until it doesn’t – remember the 2008 financial crisis?)

- Leverage – real estate is the only asset class I know of where you can lever up 20 to 1 (maybe only 10 to 1 these days given tightening mortgage requirements). To properly compare real estate to other asset classes, it is necessary to compare apples-to-apples and adjust for leverage, and other associated costs

- Forced savings plan – a lot of people who don’t have the discipline to save money are able to still do so through the purchase of a home (since the principal portion of their monthly mortgage payment is effectively savings)

A lot of people buy rental properties after doing some quick back-of-the-envelope math that may not take into account all of the considerations. I’ve tried to think through a reasonably complete list of things that you will want to think about when buying a rental property:

- I decided to use our apartment as an example to see what type of return my landlord is receiving by renting to us:

- Rental income: $1,650 / month

- What we are currently paying for a 2 bedroom + 2 bathroom condo in Edmonton, AB, Canada

- Property value: $350,000

- This is the average of three condo’s like mine in the building (based on current list price)

- To find the value of a house, I usually check out the City of Edmonton’s property tax appraisal website (https://maps.edmonton.ca/map.aspx?lookingFor=Assessments\By%20Address). The property tax appraisal value is not always equal to the market value of the property, however, is generally a good proxy

- Annual property tax: $3,264, which works out to 0.9% of the property value per year (or $272.00 / month)

- Also available online for Edmonton: http://taxestimator.edmonton.ca/

- Time horizon: Let’s assume we plan to hold this property for the long term (say 20 years). Generally a longer time horizon makes the economics more favourable since one-time costs will be amortized over a greater number of years

- Mortgage: for now let’s assume that we are using leverage since this is the norm for most real estate investors. Assumptions:

- Down payment: 20%

- Mortgage term: 25 years

- Mortgage rate: 3.50%

- I know interest rates are low right now, however, we need to consider what our borrowing costs may be over a longer term. As far as I know, unlike the US, it is quite rare to get a 25-year fixed rate mortgage in Canada

- Appreciation: let’s assume 2.0% per year (the long term Bank of Canada inflation target)

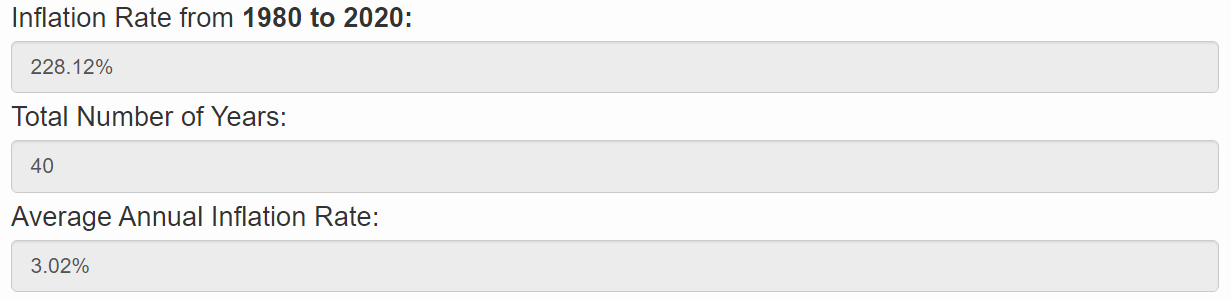

- In Edmonton, most people of my age have parents who bought a house in the 80’s for around $100,000 that is now worth around $400,000. Seeing this, you probably think to yourself – wow, 4x my money, where do I sign! But let’s dive deeper into this. If you bought a house in 1980 for $100,000 and it is worth $400,000 today, what is the actual compounded rate of increase over that 40-year period?

- The answer?

- 3.52649% BIG WHOOP

- Really?

- Yes

- How?

- Well the math based on a simple future value calculation is (1+0.0352649)^40 x $100,000 = $400,000

- The other thing to consider is that this is a nominal increase (i.e. includes the impact of inflation over time). The actual real (inflation-adjusted) increase in the value of the home is much less (especially considering that inflation was very high in the 80’s). When I ran the numbers, even I was surprised. The following numbers are from https://inflationcalculator.ca/alberta/ , however, there is also a good inflation calculator on the Bank of Canada website: https://www.bankofcanada.ca/rates/related/inflation-calculator/

- The answer?

- In Edmonton, most people of my age have parents who bought a house in the 80’s for around $100,000 that is now worth around $400,000. Seeing this, you probably think to yourself – wow, 4x my money, where do I sign! But let’s dive deeper into this. If you bought a house in 1980 for $100,000 and it is worth $400,000 today, what is the actual compounded rate of increase over that 40-year period?

- Rental income: $1,650 / month

-

-

-

- This basically shows that a $100,000 house in 1980 is equivalent to a $328,118 house today. This means that out of the 3.5% property appreciation I mentioned above, 3.0% of that was inflationary impact, leaving a real return of only 0.5%!

-

- Property management: 10% of gross rent

- I’ve read that property managers charge 8-10% of gross rents on average

- Some people choose to do this themselves, but either way, I think it is important to include something here since your time and life energy is your most valuable resource

- Maintenance costs: $497.75 / month (condo fees per the real estate posting – works out to ~1.7% per year)

- I’ve read that maintenance costs average 1-4% of the home’s value per year

- Taxes: 30% of net income, 15% capital gains tax (see disclaimer below – I am not an accountant)

- Unless held within a corporation, I believe (don’t quote me) that net income from renting out real estate (after expenses) is added to an individual’s income at their marginal tax rate

- In Canada, you will also have to pay tax on the capital gain of a real estate investment if it appreciates over time. Here I have assumed that the tax rate on capital gains is 50% of what it is on income. The actual calculation is a bit more complex but this is a good proxy

- Vacancy: 2.8%

- I’ve assumed that the house will be vacant for 1 month every 3 years

- Some people forget to consider the fact that the place may not be rented 100% of the time. Chances are once you purchase a place it will take some time to get the first tenant in and there may be some downtime between tenants

- Realtor cost to sell: 3.0%

- I’ve read that the typical range is 3-7% in Canada

- Legal costs to buy and sell: $1,000

-

Based on the assumptions above, here is the math I worked out using a Google sheets template that I built:

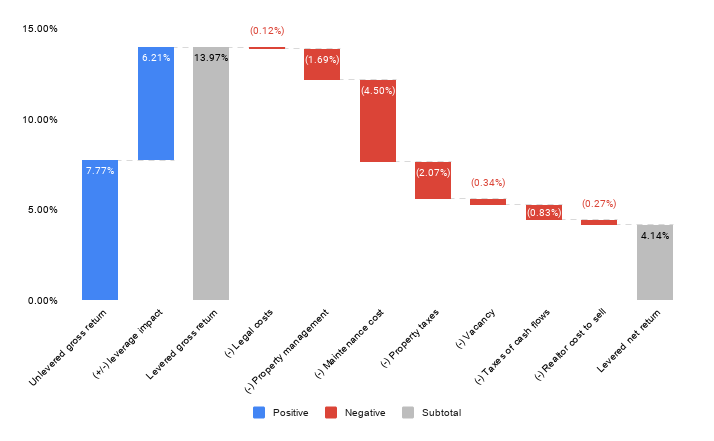

Scenario 1: Internal rate of return with 80% leverage Scenario 2: Internal rate of return without leverage (assumes 100% cash purchase)

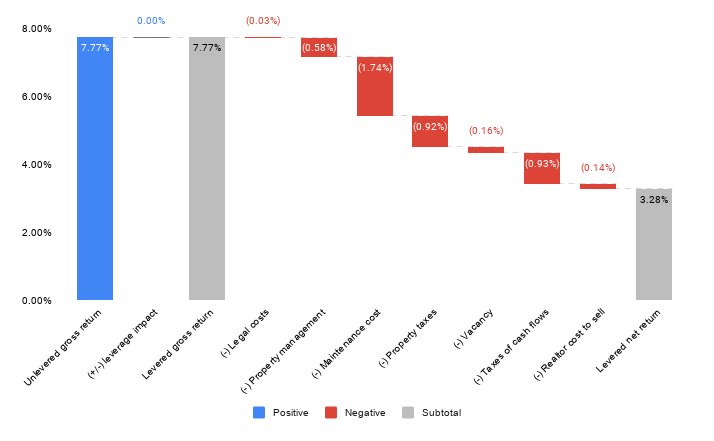

Scenario 2: Internal rate of return without leverage (assumes 100% cash purchase)

A few observations:

- The “unlevered gross” return has two key components

- Income return from gross rents (e.g. $1,650 x 12 = $19,800 / year)

- $19,800 ÷ $350,000 = 5.65%

- I have assumed that this percentage of the property value sticks (so the rent will increase in dollar terms over time to keep up with inflation)

- Appreciation return: assumed to be 2% (inflation, to be conservative)

- Income return from gross rents (e.g. $1,650 x 12 = $19,800 / year)

- Leverage has a huge impact

- As you can see, leverage is accretive to your overall returns as long as your borrowing rate is less than your expected investment return

- In the scenario with leverage, each of the costs have a bigger negative impact on overall return (since the initial investment amount funded in cash is smaller)

- Maintenance cost is the largest negative contributor to returns, however, it is often overlooked in back-of-the-envelope calculations (this is generally more front of mind with a condo investment since the condo fee is a significant monthly expense; but not as transparent with houses since they are usually more lumpy costs – e.g. roof, windows etc.)

- Taxes – in this example the tax drag is just under 1% – again, often overlooked

- Overall the nominal (includes inflation) “net” return is between 3.3% (unlevered) and 4.1% (levered)

- At a 2% inflation rate, this implies a real return of only ~1.3-2.1%

The bottom line is, if you are buying a house, I think you should run a detailed analysis of the numbers. Where I think you need to be careful:

- Leverage

- If used correctly, it can be a very powerful wealth building tool. When your expected investment return exceeds your borrowing costs, leverage can really increase your returns given you are able to capture that spread on the money that is borrowed. Additionally, interest paid on debt used to lever an investment is often tax deductible, which effectively lowers your borrowing cost on an after-tax basis (widening the spread further)

- Where I think people need to be extra careful, it to really think about their exposure in terms of total exposure (not just the cash that they need to fork out as down payment, but the total value of the property). For example, if you are buying a $400,000 home and putting 10% down, that is a $40,000 investment for you. But when you think about market exposure, all $400,000 is exposed to market fluctuations. That said, if there is a 10% market correction after you bought the $400,000 home with a 10% down payment, that entire original equity investment is gone. I question whether some real estate investors are thinking about their exposures this way (especially those who have several rental properties). A longer time horizon does generally help as it increases the likelihood that the market will recover after a downturn

- Liquidity – Some properties provide cash flow that is barely positive, or worse yet, negative cash flow. If your original assumptions change (income decreases, expense increases, or worse, both), then you could be in trouble and forced to sell at a bad time if your overall liquidity position is poor

- Income projections – Current rent does not necessarily equal future rent. When market conditions change in an area (supply and demand), the rents too will change

- Expense projections – Current expenses do not necessarily equal future expenses. If you can pass through increases in expenses to the renter then you are generally okay, however, if you can’t then your return takes a hit. For example:

- Maintenance costs could be higher than what you had originally budgeted (assuming you budgeted for maintenance in the first place)

- In the case of a condo investments, the condo fees could go up or you could get hit with a special assessment to cover a deficit in the condo’s reserve fund – this can happen when major work needs to be done to a building and the reserve fund is insufficient to cover the costs

- In the case of a house, there will be big expenses that come up every now and then. Examples would be replacing the roof, replacing the windows, replacing the furnace, updating electrical / plumbing, etc. Best to get an inspection prior to purchasing a property and estimate future capital expenditure / improvements required.

- Maintenance costs could be higher than what you had originally budgeted (assuming you budgeted for maintenance in the first place)

- Interest rate variability – As discussed above, interest rates can increase

- Appreciation projections

- I would recommend that people be conservative in their appreciation projections

- It’s good to remember that past appreciation is not an indication of future appreciation. Future appreciation will be driven by forward economic fundamentals – supply and demand of properties

- I prefer to view appreciation over and above inflation as upside rather than bake it in to the base case when buying a property

- Think about exposure in terms of your broader investment portfolio

- Obviously diversification is one of the best ways to mitigate risk in an investment portfolio. When you buy a rental property, you have to consider your market exposure as the full value of the property (not just your down payment) relative to your overall investment portfolio

- For a lot of people starting out, this number can be close to or greater than 100%. This scares me a bit and is one of the major reasons I didn’t purchase real estate in my 20’s (principal residence or rental property). I didn’t want a single rental property (a chunky illiquid investment that has significant transaction costs) to make up a large portion of my portfolio. As you get older and your net worth increases, this becomes less of a concern since real estate investments will make up a smaller percentage of your overall portfolio

What to consider when comparing real estate to traditional asset classes like stocks and bonds:

-

- Traditional asset classes (equities, fixed income) may be more volatile than real estate

- Liquidity – A market investment is more liquid and can be bought and sold instantly for a very low cost, whereas when you purchase physical real estate, it takes time and money to buy and sell

- Leverage – Don’t forget to adjust for leverage to make a proper comparison. Leverage has the ability to add to your returns but can also greatly increase the volatility of your cash flows

- Passive or active – The purchase and management of real estate is not a passive activity, it takes significantly more time and effort relative to purchasing traditional investments

In my opinion, the real estate example above does not compare too favourably to other traditional, more liquid investment alternatives. That said, the gross rent on that example was low to begin with (only 5-6% of property value). There are still markets where great real estate returns are achievable. I’ve heard of several investors being able to achieve the 1% rule (whereby the gross monthly property rent is equal to 1% of the property value, or 12% per year). I’m not saying that you shouldn’t invest in real estate. Just make sure you do your homework – run the numbers, and compare the net return to other investment options / asset classes available to you on an apples-to-apples basis.

I realize that this is one of my more technical posts – if you have any questions/thoughts or want me run the numbers for you on a potential real estate investment, feel free to reach out to me (jonathan@jbfi.ca).

Disclaimer: Please note that I am NOT a registered investment advisor and all of the above are only my opinions, NOT investment advice. When making your investment decisions, if you don’t have the expertise, make sure to consult the relevant professionals (accountants, lawyers, realtors, financial advisors, etc.).

Pingback: Housing Expense: Rent vs. Buy? – JBFI Inc.