I first learnt about compound interest as a kid. My Uncle taught me this concept while our family was visiting him and my Auntie during summer vacation. I was fascinated. I spent the rest of the week with a calculator, a pen, and paper, performing countless manual calculations on how much $1,000 would be worth in 5 years / 10 years / 20 years. Unfortunately at the time I didn’t know that there was an easy “Future Value” formula that could be used to simplify the math. The 5 minutes my Uncle took to teach me this fascinating concept completely changed my life. I went on to read my first personal finance book, “The Wealthy Barber”, and started buying Canada Savings Bonds and Canada Premium Bonds in $100 increments (I was too young to open up a brokerage account). This then gradually led me to the world of personal finance and to pursue a degree in Commerce / Finance – and eventually working in Investment Management.

Have you ever heard the saying “A dollar saved is two dollars earned”? The premise behind the saying is that you need to earn more than a dollar to save a dollar given that in order to save an after-tax dollar, you need to earn more in before-tax terms and then pay tax. Taking this a step further, I would argue that a dollar saved is even more than two dollars earned. This is because that dollar saved becomes your employee, working 24 hours a day, 7 days a week to provide you with investment income.

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.” – Albert Einstein

Let’s start with a simple example:

- Let’s say you have $1,000

- Assume you can earn a 5% rate of return on your investments

- What this $1,000 looks like in

- 5 years: $1,276

- 10 years: $1,629

- 20 years: $2,653

- 50 years: $11,467

Now a more comprehensive example (apologies in advance if your name is William):

- Supersaver Steve starts putting away $1,000 a month at age 25 and continues doing so until age 65 (40 years of saving!)

- Waitandsave William isn’t as intentional or disciplined as Steve, so he puts away $4,000 a month at age 55 and continues doing so until age 65 (10 years of saving)

Let’s again assume a 5% rate of return

- Note that they both contributed the same amount to their portfolios

- Supersaver Steve contributions = $1,000 / month x 12 months per year x 40 years = $480,000 (started earlier and contributed less per month)

- Waitandsave William contributions = $4,000 / month x 12 months per year x 10 years = $480,000 (started later and contributed more per month)

Let’s take a look at how their retirement portfolios look at age 65:

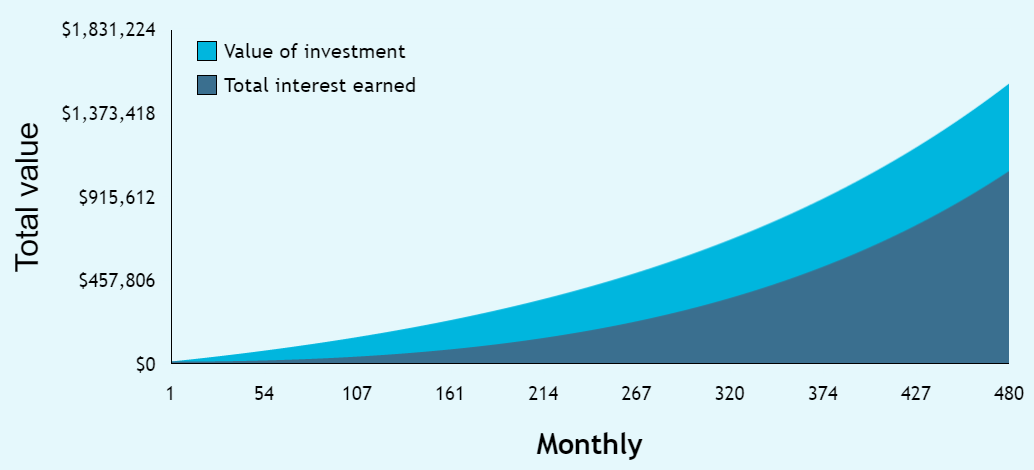

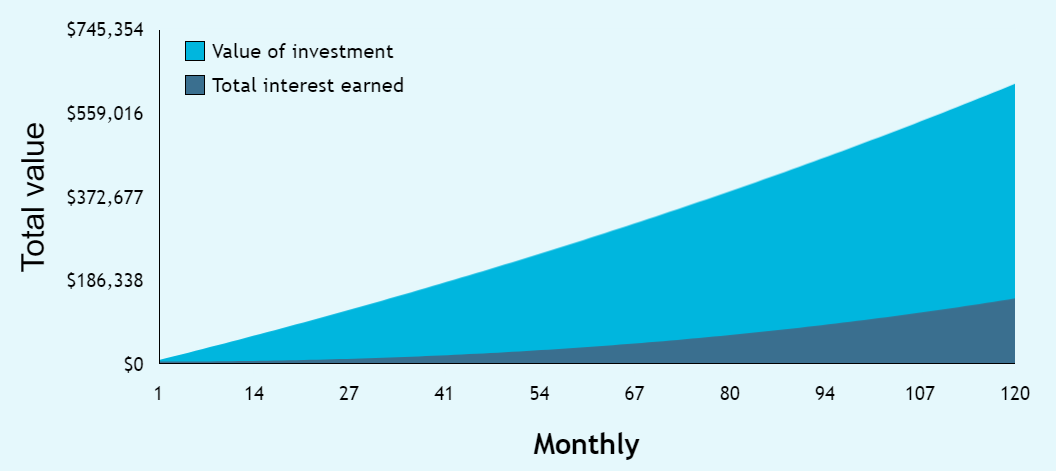

- At age 65, Waitandsave William will have $621,129

- At age 65, Supersaver Steve will have a WHOPPING $1,526,020!

Here are the charts showing the difference over time:

Supersaver Steve (starting at age 25)

Waitandsave William (starting at age 55)

A few observations and insights:

- Even though they both contributed the same total dollar amount, Supersaver Steve was able to retire with ~2.5x more since he decided to start early (he made his savings work longer and harder for him)

- Waitandsave William’s final retirement balance exceeds his contributions by a mere $141,129, whereas Supersaver Steve’s final retirement balance exceeds his contributions by a WHOPPING $1,046,020

- This is the magic of compound interest (shown in darker blue on the charts above)

- If Waitandsave William wanted to catch up and match Supersaver Steve’s retirement amount of $1,526,020 (all else equal), he would need to save $9,827 (vs. $4,000 in the original example) per month between age 55 and 65. In this case, here’s how Steve and William’s savings and interest income stack up:

| WaitandSave William | SuperSaver Steve | |

| Savings | $1,179,240 | $480,000 |

| Investment Income | $346,780 | $1,046,020 |

| Total | $1,526,020 | $1,526,020 |

The table clearly illustrates that if you don’t start putting your money to work early, you’ll have to work significantly harder in the later years to catch up – all due to compound interest!

If you don’t feel like doing the math yourself, why not run some numbers of your own using the following compound interest calculator:

Potential upside:

- We’ve been quite conservative here. There is a tonne of potential upside in these calculations. Imagine if the return on your investment is greater than 5% – instead of ending up with $1,526,020 in the example above, Supersaver Steve would have ended up with:

- $1,991,491 if he made 6%

- $2,624,813 if he made 7%

- $3,491,008 if he made 8%

- $4,681,320 if he made 9%

- $6,324,080 if he made 10%

Lessons of this post:

- Teach your kids about compound interest, it could change their lives!

- Make sure compound interest is working for you (compounding savings and investment income), rather than against you (compounding debt and interest payments)

- Start early to enjoy the benefits of compounding: the best time to start would have been 10 years ago but the second best time is TODAY!

- Think of where your investment portfolio could end up if you are able to save more than $1,000 a month! Anyone can!

Wealth, like a tree, grows from a tiny seed. The first copper you save is the seed from which your tree of wealth shall grow. The sooner you plant that seed the sooner shall the tree grow. And the more faithfully you nourish and water that tree with consistent savings, the sooner may you bask in contentment beneath its shade.

– George S. Clason, The Richest Man in Babylon